Implementing the CSRD

The Ministry of Finance has drafted a bill amending the Accounting Act, the Act on Statutory Auditors, Audit Firms and Public Supervision and certain other acts (the “Amendment”). The new draft will implement the following pieces of EU law into the Polish national legal order:

- Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014 Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU regarding corporate sustainability reporting (“CSRD”);

- Commission Delegated Directive (EU) 2023/2775 of 17 October 2023 amending Directive 2013/34/EU of the European Parliament and of the Council as regards the adaptation of the enterprise size criteria for micro, small, medium-sized and large undertakings or groups (Official Journal of the EU Law of 21.12.2023) (“Delegated Directive”).

The Amendment is at the stage of the government legislative process (RCL print: UC14),. Agreements, public consultations and opinions are currently underway. According to the List of Legislative and Programme Works of Poland’s Council of Ministers, the government plans to adopt the bill in Q2 2024.

CSRD

The CSRD (Corporate Sustainability Reporting Directive) entered into force in January 2023. The first entities are required to report under it in 2025 (using data from the 2024 financial year). The CSRD amends the reporting requirements set out in the Non-Financial Reporting Directive (the “NFRD” or Directive 2014/95/EU7), which was adopted in 2014 and came into force in 2017, following its implementation by the Polish Accounting Act. Its objective is to:

- increase the quality, comparability and reliability of non-financial data disclosed;

- ensure that sustainability reporting stands on a par with financial reporting;

- align the Directive with legislative changes in support of the EU Sustainable Finance Strategy (e.g. Taxonomy and SFDR).

The CSRD introduces new provisions which significantly expand the types of companies in the EU which are obliged to report on environmental protection, social responsibility and respect for human rights. It also changes the scope of such reporting. Both the material scope and the subject matter of the legislation are, therefore, changing.

Member states have been obliged to implement the directive into national law by 6 July 2024.

To date, the existing NFRD imposed ESG reporting obligations on around 12,000 companies in the EU. Once the CSRD enters into force, it is estimated that such obligations will apply to around 50,000 companies in the EU, including over 3,500 Polish companies.

Principles of the law implementing the CSRD

- The expanded range of reporting entities: The Amendment applies to large entities, holding companies, small and medium-sized regulated entities (SMEs), and EU subsidiaries and branches subject to third-country regulation.

- Uniform reporting standards: Rather than permitting a variety of reporting standards, the Amendment makes it mandatory to use the European Sustainability Reporting Standards (ESRS).

- Broadened information scope: More detailed information on environmental, social (including human rights) and corporate governance aspects will be required.

- Separate section in reports: Sustainability reporting will be presented in a separate section within financial statements.

- Verification by auditors: The new legislation makes it compulsory for auditors to review sustainability reports.

- Digitisation: entities’ sustainability reports will have to be in XHTML format and sustainability sections labelled using the Inline XBRL format, to facilitate machine analysis of the data.

Proposed amendments to the Accounting Act

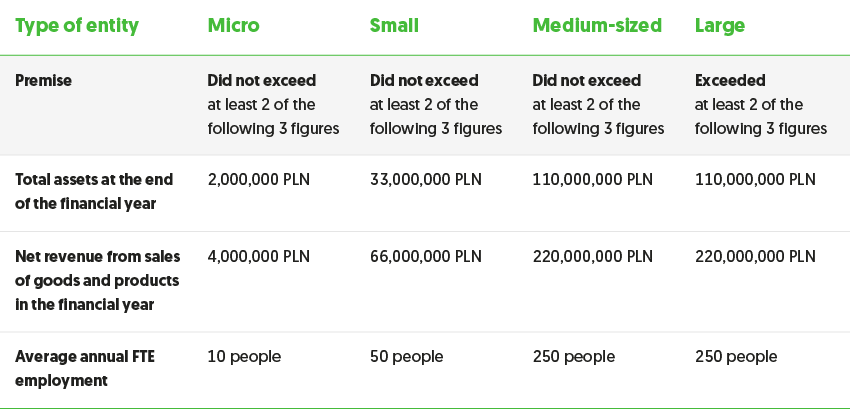

New thresholds for defining entities

The introduction of a new Chapter 6c to the Accounting Act by means of Article 1(22) of the Amendment also deserves special attention. This chapter is an essential part of CSRD implementation with respect to its sustainability reporting provisions. This new chapter imposes sustainability reporting obligations on a number of entities, including large holding companies, small and medium-sized enterprises listed on a regulated market, and subsidiaries and branches based in Poland whose ultimate parent company or stand-alone entity is governed by the laws of a third country. This key change is an important step towards implementing sustainability standards in Polish law. It ensures more comprehensive and transparent reporting of information on environmental, social and corporate governance aspects.

Entry into force of the Amendment

The Amendment enters into force 14 days after its publication date, subject to the exceptions indicated.

It should be emphasised that the Amendment will first apply to non-financial disclosures related to 2024 (reporting takes place in 2025) for the largest public interest entities (e.g. listed companies, banks and insurers) and public interest institutions that are parent companies of the largest groups. These will be the first sustainability reports drawn-up under the new rules.

Recent news

Efektywne zarządzanie emisjami: ISO 14064 i ISO 14067

Ważnym aspektem zrównoważonego rozwoju jest efektywne zarządzanie i redukcja emisji gazów cieplarnianych. Wśród narzędzi wykorzystywanych do tego celu najczęściej stosowane są GHG Protocol, raporty IPCC oraz normy ISO. W poniższym artykule przybliżymy aspekty dotyczące ISO 14064 i ISO 14067, które oferują firmom i organizacjom spójne ramy do identyfikacji, pomiaru i raportowania śladu węglowego na poziomie zarówno organizacji, jak i produktu.

Modernizacja budynków: Wpływ dyrektywy EPBD na rynek nieruchomości

Rynek nieruchomości jest jednym z głównych konsumentów energii energetycznej, odpowiadając za około 40% globalnych emisji CO21. Według najnowszych statystyk 85% budynków w UE powstało przed rokiem 2000, a 75% z nich charakteryzuje się niską efektywnością energetyczną2. Z tego względu jest to sektor szczególnie znaczący, który wymaga pilnego działania by zmniejszyć jego negatywny wpływ na środowisko.

Konferencja „Ślad węglowy – Raport z badania polskich przedsiębiorstw”

Zespół Greeners, SSW oraz Konfederacja Lewiatan serdecznie zapraszają na konferencję „Ślad węglowy – Raport z badania polskich przedsiębiorstw”, która odbędzie się 1 kwietnia 2025 r. w Warszawie (Rondo ONZ 1, p. 12). Podczas wydarzenia zaprezentujemy wyniki naszego badania ankietowego, a także zaprosimy Państwa do udziału w dwóch panelach dyskusyjnych z udziałem ekspertów i przedstawicieli biznesu.

Energy transition of your company

We specialize in implementing sustainable development solutions that deliver tangible benefits to our clients.